VAR Modeling

library(vars)

# Generated Time Series

x1 = 10 + arima.sim(n = 100,model = list(order = c(1, 1, 1), ar = .1, ma = .2))

x2 = 10 + arima.sim(n = 100,model = list(order = c(1, 1, 1), ar = .1, ma = .2))

x3 = 10 + arima.sim(n = 100,model = list(order = c(1, 1, 1), ar = .1, ma = .2))

x4 = 10 + arima.sim(n = 100,model = list(order = c(1, 1, 1), ar = .1, ma = .2))

# Combine into a multivariate time series

x = data.frame(x1, x2, x3, x4)

# Create a variable auto-regression modle

mdl = VAR(x)

# Model summary

summary(mdl)

VAR Estimation Results:

=========================

Endogenous variables: x1, x2, x3, x4

Deterministic variables: const

Sample size: 100

Log Likelihood: -554.174

Roots of the characteristic polynomial:

1.001 0.9732 0.9732 0.8473

Call:

VAR(y = x)

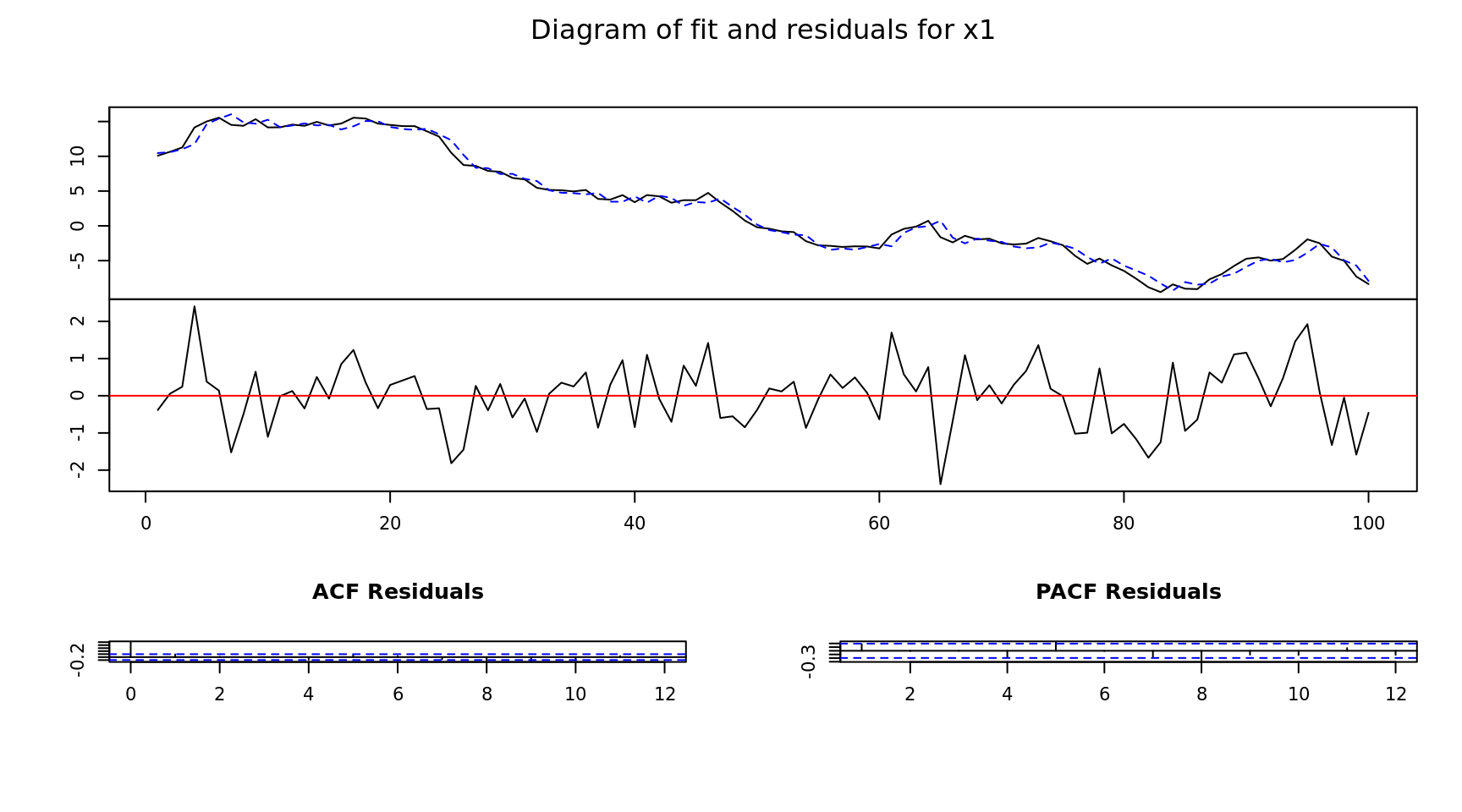

Estimation results for equation x1:

===================================

x1 = x1.l1 + x2.l1 + x3.l1 + x4.l1 + const

Estimate Std. Error t value Pr(>|t|)

x1.l1 0.963228 0.018160 53.040 < 2e-16 ***

x2.l1 0.075584 0.031008 2.438 0.01665 *

x3.l1 0.143179 0.043729 3.274 0.00148 **

x4.l1 0.007627 0.017186 0.444 0.65822

const -1.425166 0.584460 -2.438 0.01661 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.868 on 95 degrees of freedom

Multiple R-Squared: 0.9881, Adjusted R-squared: 0.9876

F-statistic: 1971 on 4 and 95 DF, p-value: < 2.2e-16

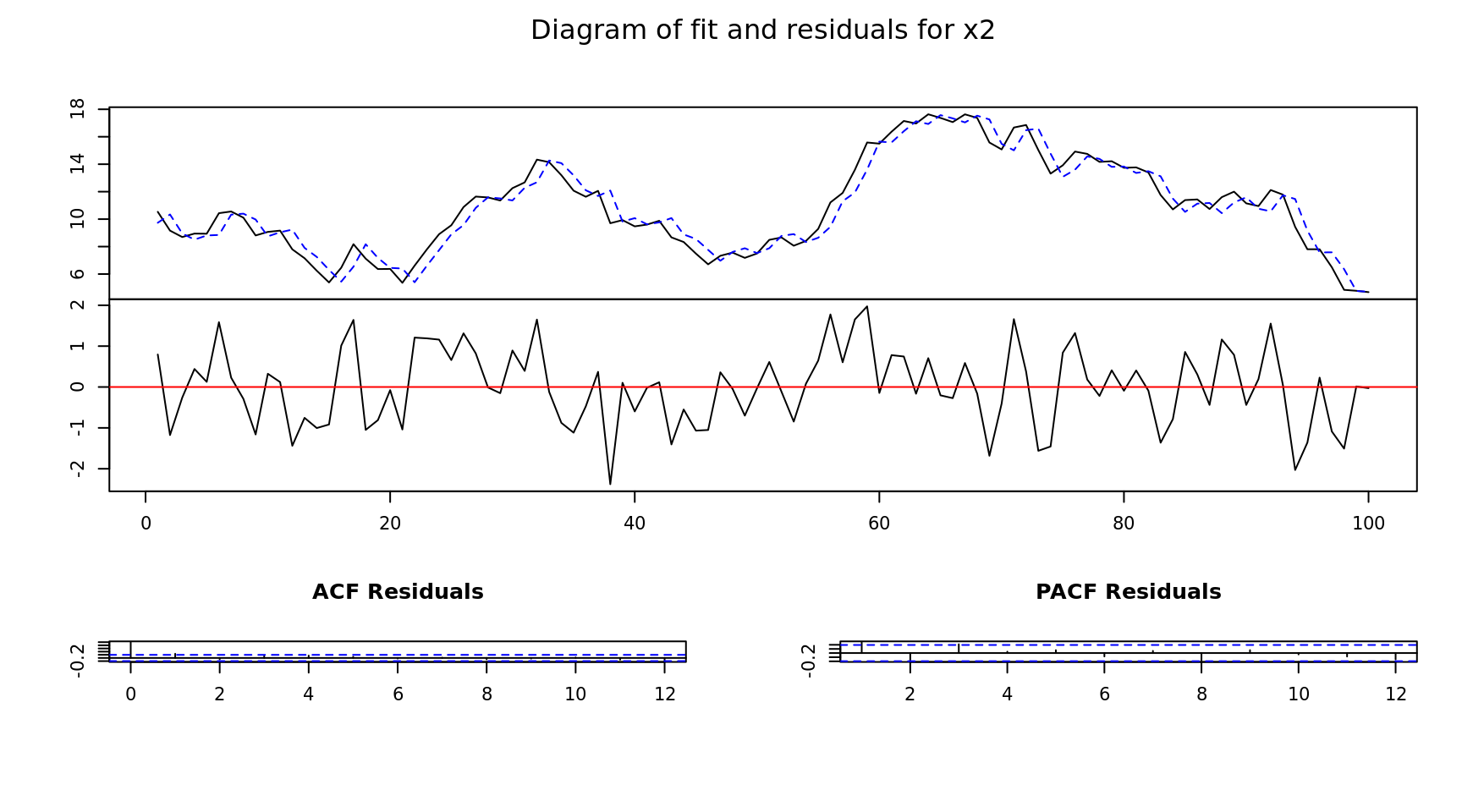

Estimation results for equation x2:

===================================

x2 = x1.l1 + x2.l1 + x3.l1 + x4.l1 + const

Estimate Std. Error t value Pr(>|t|)

x1.l1 -0.001462 0.019970 -0.073 0.942

x2.l1 0.972519 0.034098 28.521 <2e-16 ***

x3.l1 0.025001 0.048087 0.520 0.604

x4.l1 0.031043 0.018899 1.643 0.104

const -0.535590 0.642706 -0.833 0.407

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9545 on 95 degrees of freedom

Multiple R-Squared: 0.9251, Adjusted R-squared: 0.9219

F-statistic: 293.2 on 4 and 95 DF, p-value: < 2.2e-16

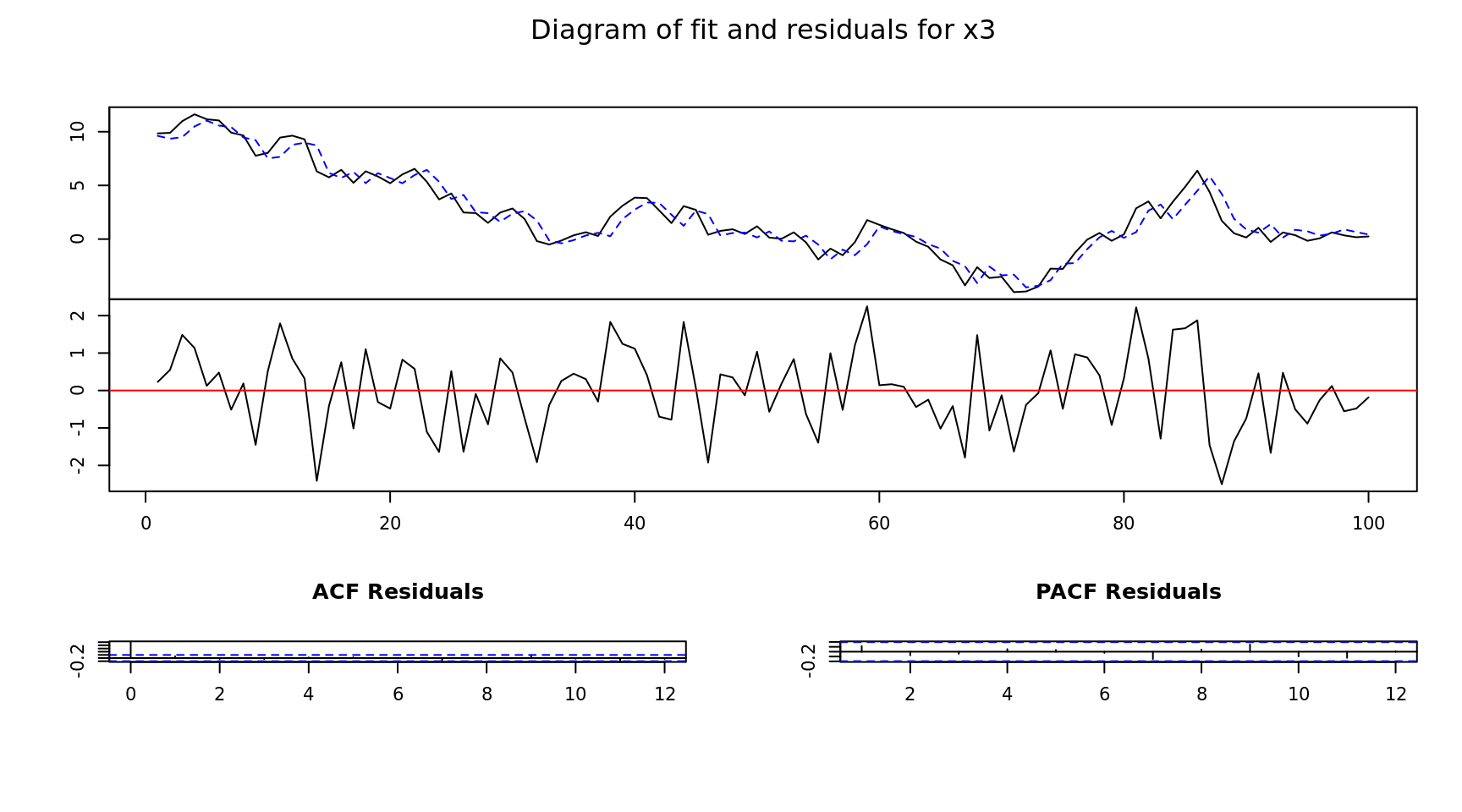

Estimation results for equation x3:

===================================

x3 = x1.l1 + x2.l1 + x3.l1 + x4.l1 + const

Estimate Std. Error t value Pr(>|t|)

x1.l1 0.02503 0.02235 1.120 0.2656

x2.l1 -0.01399 0.03816 -0.367 0.7147

x3.l1 0.85840 0.05381 15.951 <2e-16 ***

x4.l1 -0.04462 0.02115 -2.110 0.0375 *

const 1.36738 0.71927 1.901 0.0603 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.068 on 95 degrees of freedom

Multiple R-Squared: 0.929, Adjusted R-squared: 0.926

F-statistic: 310.8 on 4 and 95 DF, p-value: < 2.2e-16

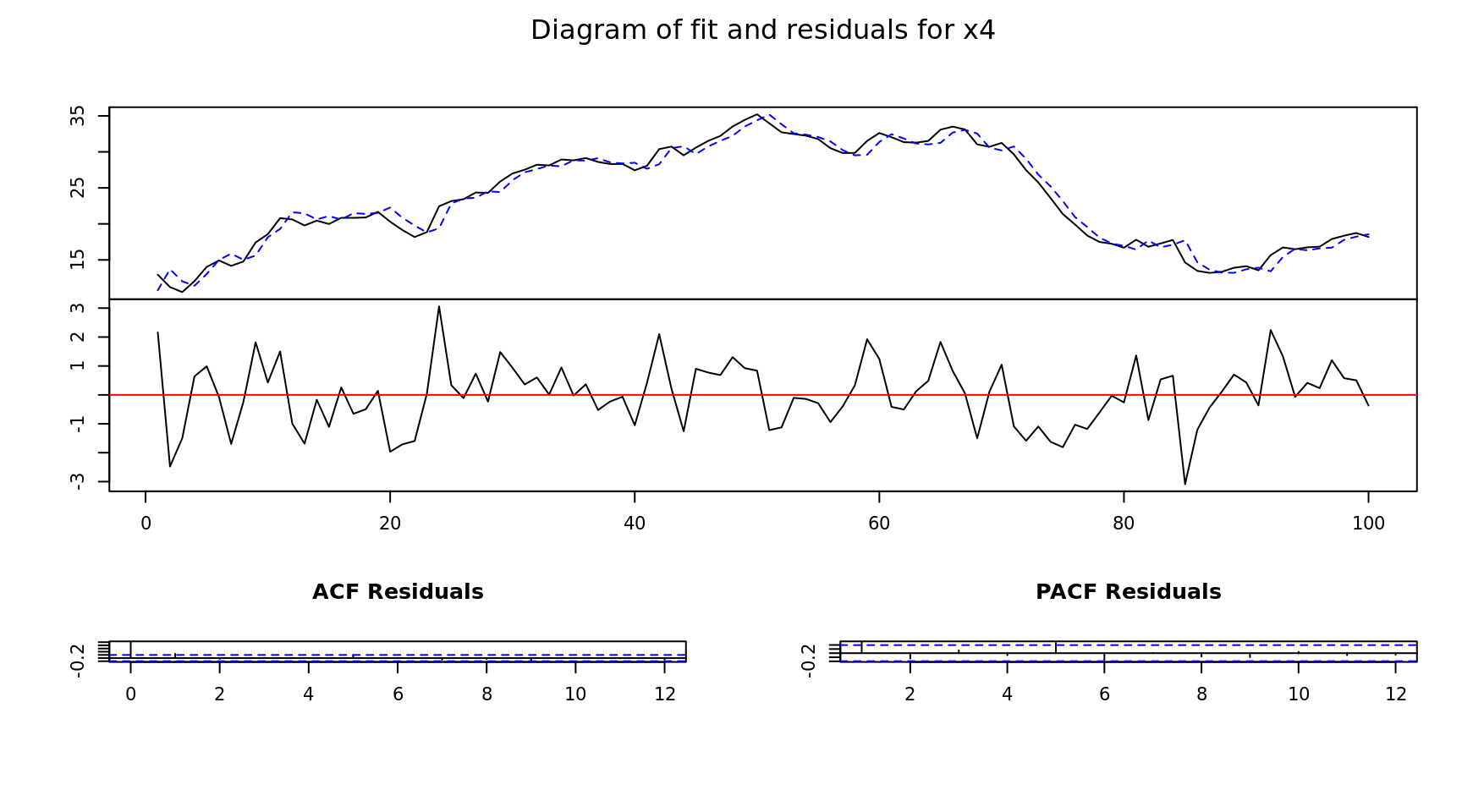

Estimation results for equation x4:

===================================

x4 = x1.l1 + x2.l1 + x3.l1 + x4.l1 + const

Estimate Std. Error t value Pr(>|t|)

x1.l1 0.01831 0.02364 0.774 0.441

x2.l1 -0.01214 0.04037 -0.301 0.764

x3.l1 0.07116 0.05693 1.250 0.214

x4.l1 0.99872 0.02238 44.633 <2e-16 ***

const 0.02153 0.76094 0.028 0.977

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.13 on 95 degrees of freedom

Multiple R-Squared: 0.9751, Adjusted R-squared: 0.9741

F-statistic: 930 on 4 and 95 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

x1 x2 x3 x4

x1 0.75349 -0.09141 -0.01242 -0.05868

x2 -0.09141 0.91116 -0.06800 0.08389

x3 -0.01242 -0.06800 1.14116 -0.23538

x4 -0.05868 0.08389 -0.23538 1.27722

Correlation matrix of residuals:

x1 x2 x3 x4

x1 1.00000 -0.11032 -0.01339 -0.05981

x2 -0.11032 1.00000 -0.06669 0.07777

x3 -0.01339 -0.06669 1.00000 -0.19497

x4 -0.05981 0.07777 -0.19497 1.00000